Financiële resultaten Renault Group in H1 2025: een stevig fundament voor tweede helft 2025

Renault Group presenteert solide financiële resultaten over de eerste helft van 2025, met een omzetstijging van 2,5 procent en een operationele marge van 6,0 procent. Zonder de impact van het belang in Nissan noteert Renault Group een nettowinst van 461 miljoen euro.

- Groepsomzet: 27,6 miljard euro, +2,5% en +3,6% bij constante wisselkoersen1 ten opzichte van H1 2024

- Omzet autodivisie: 24,5 miljard euro, +0,5% en +1,6% bij constante wisselkoersen1 ten opzichte van H1 2024

- Operationele marge van Renault Group: 1,7 miljard euro, oftewel 6,0% van de groepsomzet

- Operationele marge van autodivisie: 1,0 miljard euro, oftewel 4,0% van de automotive-omzet

- Nettoresultaat: 0,5 miljard euro, exclusief het effect van Nissan2

- Effect Nissan: -11,6 miljard euro

- -2,3 miljard euro in de bijdrage van geassocieerde ondernemingen

- -9,3 miljard euro niet-geldelijk verlies als gevolg van de wijziging in de boekhoudkundige verwerking van de investering in Nissan

- Vrije kasstroom3: 47 miljoen euro, inclusief 150 miljoen euro aan dividend van Mobilize Financial Services (vergeleken met 600 miljoen euro in H1 2024), met een negatieve verandering in werkkapitaalbehoefte van -897 miljoen euro

- Netto kaspositie autodivisie: 5,9 miljard euro per 30 juni 2025

- Commerciële prestaties van automerken van Renault Group:

- Renault

- In Europa4: #2 in personen- en lichte bedrijfswagens (PC+LCV5), met de Clio als bestverkochte model, #2 in hybride voertuigen (HEV)

- In Frankrijk: #1 in PC+LCV5, #1 in elektrische voertuigen (EV) en #1 in personenwagens HEV in Europe1

- Dacia in Europa: in de top 10 van bestverkochte merken, #3 in particuliere verkoop personenwagens (retail PC), met de Sandero als bestverkochte personenauto over alle verkoopkanalen en de Duster als bestverkochte SUV in de particuliere markt

- Alpine: +85% verkoopgroei ten opzichte van H1 2024

- Renault

- Sterk orderboek in Europa, gelijk aan twee maanden vooruitverkoop, wijst op een sterke orderinstroom dankzij succesvolle modelintroducties

- Gezond voorraadniveau: 530.000 voertuigen per 30 juni 2025

- Financiële vooruitzichten voor 2025 (bijgewerkt op 15 juli 2025):

- Operationele marge groep rond de 6,5%

- Vrije kasstroom tussen 1,0 en 1,5 miljard euro

Het vervolg van dit persbericht gaat verder in het Engels

“As I step into the role of CEO, I am convinced that Renault Group has all the fundamentals to succeed: committed teams, a robust product plan, a clear brands’ positioning, and an innovative organization.

Our first-half results, in a challenging market, were not aligned with our initial ambitions. We have already launched a set of countermeasures to deliver our targets. Nevertheless, Renault Group’s profitability remains a reference in our industry, and we are determined to maintaining this standard.

The roadmap is clear: ensure continuity in our strategy while accelerating our transformation.

In a highly disruptive environment, we concentrate on what we control: energizing our teams, prioritizing investment on products, delivering best-in-class performance, and leveraging our unique network of partners. I am convinced that Renault Group is well-positioned to deliver sustainable, best-in-class value for the years to come.” said François Provost, CEO of Renault Group

Boulogne-Billancourt, July 31, 2025

Financial results

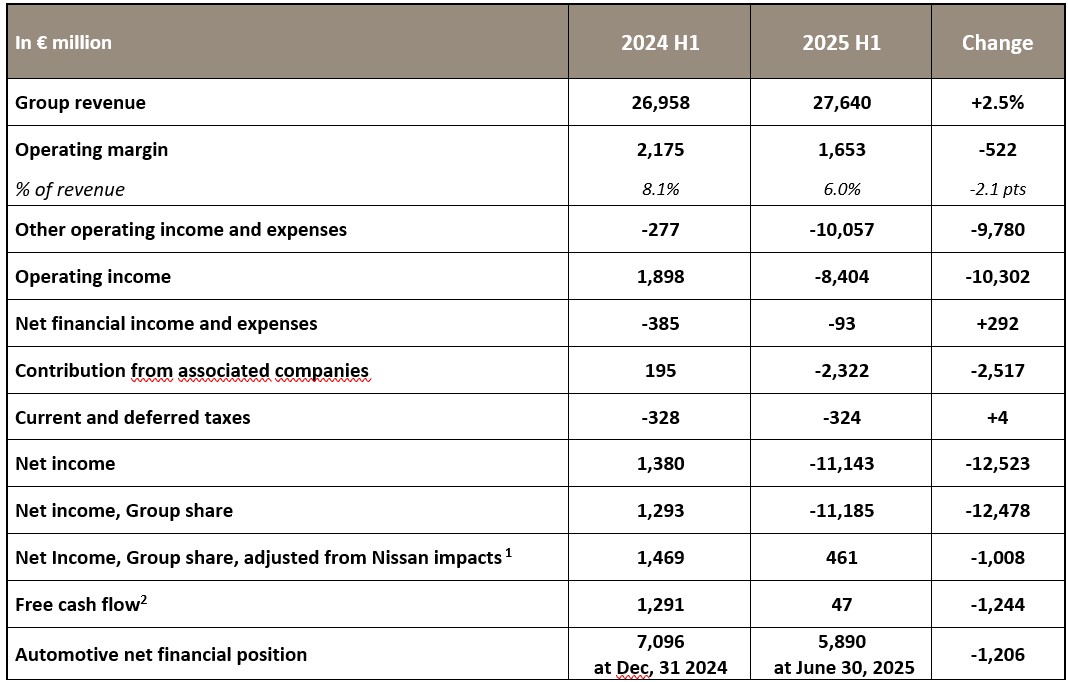

Group revenue reached €27,640 million, up 2.5% compared to 2024 H1. At constant exchange rates⁶, it increased by 3.6%.

Automotive revenue stood at €24,490 million, up 0.5% compared to 2024 H1. It included -1.1 points of negative exchange rates effect (-€264 million) mainly related to the devaluation of the Turkish lira, Brazilian real and Argentinean peso. At constant exchange rates⁶, it increased by +1.6%. This evolution was mainly explained by the following:

- A positive volume effect of +1.1 points. The 1.3% increase in registrations was partially offset by a higher destocking within the dealership network in 2025 H1 compared to 2024 H1. Last year destocking was quite low notably in the context of the transition to the new GSR⁷. As of June 30, 2025, total inventories of new vehicles stood at a healthy level and represented 530,000 vehicles, of which 416,000 vehicles at independent dealers and 114,000 at Group level.

- A positive product mix effect of +3.3 points thanks to our recent launches (Bigster, Duster, Symbioz, Renault 5, A290, Grand Koleos, Rafale…). This positive effect will continue to improve in the coming semester.

- A neutral price effect despite a challenging environment in Europe, marked by the decline in the retail market and a sharply declining LCV market, which led to an increasing commercial pressure. Outside Europe, most of the negative currency impact is offset by price increases.

- A negative geographic mix of -1.1 points, mainly explained by the growth of sales outside Europe.

- A negative effect of sales to partners of -1.9 points. This evolution is primarily explained by the one-off R&D billings to partners in H1 2024, the deconsolidation of Horse’s powertrains sales to partners at the end of May 2024, and the decrease of vehicles sales to partners ahead of the forthcoming launches of new models (e.g. Nissan Micra, Mitsubishi C-SUV, Polestar 4).

- An “Other” effect of +0.2 points.

The Group posted an operating margin of €1,653 million or6.0% of revenue versus 8.1% in 2024 H1.

Automotive operating margin stood at€989 million versus €1,600 million in 2024 H1. It represented 4.0% of Automotive revenue, versus 6.6% in 2024 H1. This evolution was mainly explained by the following:

- An impact of foreign exchange of -€25 million, the positive impact of the Turkish lira devaluation on production costs offsetting the negative impact of devaluations on revenue.

- A positive volume effect of +€48 million.

- Price/mix/enrichment effect stood at -€444 million mainly due to the combination of a negative mix effect, with a lower share of LCVs and higher share of EVs, alongside the commercial pressure. Costs were reduced by €287 million thanks to a strong purchasing performance and to a lesser extent to a raw materials tailwind.

Renault Group continues to reduce its costs and to pass part of those gains to its customers which allows the Group to boost its competitiveness by offering attractive vehicles in terms of price and content while offsetting regulatory requirements, especially on new models and facelifts. Renault Group’s strategy is to work on the combination of these two effects, with the sole objective of improving competitiveness. This combined effect should be a positive for the full year, supported notably by the purchasing performance and raw materials tailwind. The purchasing performance is starting to benefit from the synergies on powertrains delivered by Horse. - R&D posted a negative impact of -€166 million, primarily due to an unfavorable comparison base in 2024 H1 with non-recurring R&D billings to partners.

- SG&A improved by +€16 million.

- “Others” effect stood at -€34 million.

- Prior to deconsolidation on May 31st, 2024, Horse was under the IFRS 5 assets held for sale accounting treatment and therefore, amortization of its assets had been suspended. Since Horse was deconsolidated, invoices paid to Horse by Renault Group include the cost of amortization as well as Horse’s mark up. These two cumulated effects represented a negative impact of -€279 million in 2025 H1 compared to 2024 H1.

The contribution of Mobilize Financial Services (Sales Financing) to the Group’s operating margin reached €668 million, up €75 million vs. 2024 H1, mainly thanks to the continuous strong growth of the customer financing activity as well as the positive margin evolution.

Other operating income and expenses were negative at -€10.1 billion (vs -€0.3 billion in 2024 H1). It mainly included the non-cash loss linked to the change of the accounting treatment of Renault Group’s stake in Nissan for -€9.3 billion⁸ (cf press release of July 1, 2025).

It corresponded to the difference between the present carrying value of the investment and the fair value based on Nissan’s stock price as of June 30, 2025, plus notably the impact of the recycling of conversion reserves and net investment hedges related to Nissan’s equity accounted securities.

This loss is non-cash and has no impact on the calculation of the dividend paid by Renault Group.

The benefit of this evolution is that, from now on, any change in the fair value of the stake in Nissan based on Nissan’s stock price, will be directly recognized in equity, with no impact on Renault Group’s net income. Renault Group will continue to benefit from any dividends that Nissan may pay in the future.

After considering other operating income and expenses, the Group’s operating income stood at

-€8,404 million compared to €1,898 million in 2024 H1.

Net financial income and expenses amounted to -€93 million compared to -€385 million in 2024 H1. This variation is mostly explained by the negative impact of hyperinflation in Argentina in 2024 H1.

The contribution of associated companies amounted to -€2,322 million compared to €195 million in 2024 H1. It included -€2,331 million of Nissan’s negative contribution (-€2,204 million in Q1 and

-€127 million in Q2).

Current and deferred taxes represented a charge of -€324 million, including -€24 million related to the French exceptional surtax, compared to a charge of -€328 million in 2024 H1. The effective tax rate was impacted by the 2025 losses in France.

Thus, net income stood at -€11,143 million in 2025 H1. Net income, Group share, was -€11,185 million

(or -€40.90 per share). Net income, Group share, excluding Nissan impacts⁹ was €461 million

(or €1.69 per share).

The cash flow of the Automotive business reached €2,045 million in 2025 H1 and included

€150 million of Mobilize Financial Services dividend (vs €600m in 2024 H1) and restructuring costs for -€116 million.

Excluding the impact of asset disposals, the Group’s net CAPEX and R&D stood at €1,932 million

i.e. 7.0% of revenue compared to 7.9% of revenue in 2024 H1. Assets disposals amounted to

€42 million, compared to €28 million in 2024 H1. Group’s net CAPEX and R&D amounted to 6.8% of revenue including asset disposals.

Free cash flow¹⁰ stood at €47 million. It included a negative change in working capital requirement of -€897 million, mainly related to the level of production at the end of 2024 higher than at the end of June 2025 and to a higher Group inventories level compared to the end of December 2024 which was at a particularly low level. However, total inventories (Group and independent dealers) stood at 530,000 vehicles at the end of June, down compared to March 2025 (560,000 vehicles).

The Automotive net cash financial position stood at €5,890 million on June 30, 2025, compared to €7,096 million on December 31, 2024. This evolution was driven by dividends paid to shareholders for -€693 million and net financial investments for -€173 million, mainly in Free To X (a subsidiary of Autostrade per l’Italia operating a fast charge network in Italy).

Liquidity reserve at the end of June 2025 stood at a high level at €15.8 billion.

2025 FY financial outlook

In order to take into account the deterioration of the automotive market trends with an increasing commercial pressure from its competitors and the anticipation of the continuation of the retail market decline, Renault Group has updated its 2025 financial outlook on July 15, 2025:

- Group operating margin around 6.5%

- Free cash flow between €1.0bn and €1.5bn

The Group has a clear roadmap to confirm H2 performance above H1 thanks to the following levers:

- Higher volume effect in H2 vs H1:

- Strong level of orders in June

- Effect of the ramp-up of launches

- Increased sales to partners

- Discipline and strict control on variable and fixed costs.

The combined effect of price/mix/enrichment and costs should be a positive for H2 and full year operating margin.

Renault Group is pursuing its strict commercial policy, prioritizing value creation over volume to protect the residual value of vehicles. Renault Group is also strengthening its short-term costreduction planand accelerating on its initiatives with more structural levers (SG&A cost reduction, manufacturing and R&D savings).

To meet the challenges of an increasingly competitive market, Renault Group can rely on its strong fundamentals:

- A flexible and agile business model to meet market demands for combustion, hybrid and electric vehicles, whatever the pace of the energy transition;

- An attractive line-up for European and international markets, supported by 7 launches and

2 facelifts in 2025 to complement the 10 launches and 2 facelifts in 2024; - A focus on the most profitable channel of sales to retail customers in Europe (c. +15 points above market average);

- A continuous vehicle cost reduction;

- A rigorous approach to residual values, 4 to 13 points higher than European peers;

- A strong orderbook in Europe, representing two months of sales, reflecting the success of the products;

- A healthy management of inventories;

- A high plant utilization rate, around 90% on average.

Renault Group’s consolidated results

(1) H1 2024: +€264m positive contribution in associated companies, -€440 million capital loss on the disposal of Nissan shares.

H1 2025: -€2,331m negative contribution of associated companies, and -€9,315 million loss resulting from the evolution of the accounting treatment for the investment in Nissan.

(2) Free cash flow: cash flows after interest and tax (excluding dividends received from publicly listed companies) minus tangible and intangible investments net of disposals +/- change in the working capital requirement, and minus cash flows relating to material non-recurring and long-standing litigations.

From 2025 onwards, cash flows relating to material non-recurring and long-standing litigationswill be excluded from free cash flow, in order to better reflect cash flows of the ordinary activities of the Automotive business. Payments made in respect of such flows represent -83 million euros at end-June 2025 and mainly relate to settlements of tax litigations from previous financial years. Free cash flow for 2024 H1 has been restated accordingly and increased by 34 million euros.

Additional information

The condensed half-year consolidated financial statements of Renault Group at June 30, 2025 were reviewed by the Board of Directors on July 30, 2025.

Limited review procedures were completed with respect to the condensed consolidated half-year financial statements, and an unqualified review report has been issued by the statutory auditors.

The financial report, with a complete analysis of the financial results in the first half of 2025, is available at www.renaultgroup.com in the “Investors” section.

2025 H1 Financial Results Conference

Link to follow the conference on July 31, 2025, from 8am CEST and available in replay:

[1] In order to analyze the variation in consolidated revenue at constant exchange rates, Renault Group recalculates the revenue for the current period by applying average exchange rates of the previous period.

[2] H1 2025: -€2,331m negative contribution of associated companies, and -€9,315m loss resulting from the evolution of the accounting treatment for the investment in Nissan.

[3] See free cash flow full definition and change of methodology at “2 -” under the table of Renault Group’s consolidated results.

[4] Europe ACEA scope.

[5] Passenger cars and light commercial vehicles.

[6] In order to analyze the variation in consolidated revenue at constant exchange rates, Renault Group recalculates the revenue for the current period by applying average exchange rates of the previous period.

[7] GSR: EU General Safety Regulation.

[8] Based on Nissan’s stock price of JPY350 and a EUR/JPY exchange rate of 169.

[9] Nissan’s impacts in 2025 H1: -€2,331m of Nissan’s negative contribution in associated companies, -€9,315m loss resulting from the evolution of the accounting treatment for the investment in Nissan recorded in other income and expenses.

[10] See free cash flow full definition and change of methodology at “2 -” under the table of Renault Group’s consolidated results.