Renault Group toont veerkracht, de robuustheid van zijn strategie en gaat vol vertrouwen vooruit

Renault Group heeft in 2025 een sterke winstgevendheid en kasstroom gerealiseerd en daarmee voldaan aan de financiële verwachtingen die op 15 juli 2025 werden geüpdatet.

- Groepsomzet: €57,9 miljard, +3,0% en +4,5% bij constante wisselkoersen1 ten opzichte van 2024. Deze robuuste prestatie werd gedreven door de complementaire automerken van Renault Group, die alle drie groei realiseerden dankzij de uitrol van het International Game Plan en de elektrificatie van het modellenaanbod

- Sterke operationele marge Renault Group: €3,6 miljard, goed voor 6,3% van de groepsomzet

- Nettoresultaat: -€10,9 miljard, inclusief het effect van Nissan: een niet-geldelijke verliespost van

-€9,3 miljard als gevolg van de wijziging in de boekhoudkundige verwerking van de investering in Nissan en -€2,3 miljard uit de bijdrage van geassocieerde ondernemingen - Sterke vrije kasstroom autodivisie2: €1,5 miljard, gedreven door de operationele prestaties van Renault Group, deels gecompenseerd door de negatieve verandering in de werkkapitaalbehoefte. Dit omvatte €300 miljoen aan ontvangen dividend van Mobilize Financial Services.

- Netto kaspositie autodivisie: €7,4 miljard per 31 december 2025

- Gezond voorraadniveau: 539.000 voertuigen per 31 december 2025.

- Een dividend van €2,20 per aandeel wordt ter goedkeuring voorgelegd aan de Algemene Vergadering op 30 april 2026.

- Verbetering van kredietwaardigheid: S&P Global Ratings heeft Renault SA op 18 december 2025 van ‘BB+’ opgewaardeerd naar een lange termijn investment grade kredietrating ‘BBB-’ met stabiel vooruitzicht

- Financiële vooruitzichten 2026: veerkracht in een complexe omgeving

- Operationele marge Renault Group: rond 5,5% van de groepsomzet

- Vrije kasstroom autodivisie: rond €1 miljard, inclusief €350 miljoen dividend van Mobilize Financial Services3

- Financiële vooruitzichten op middellange termijn: robuuste en veerkrachtige financiële resultaten behouden:

- Operationele marge Renault Group: tussen 5% en 7% van de groepsomzet op middellange termijn. De ondergrens van de margeprognose ligt aanzienlijk boven de historische marges4

- Vrije kasstroom autodivisie: gemiddeld ≥€1,5 miljard per jaar op middellange termijn5, inclusief een gemiddelde van circa €500 miljoen dividend³ per jaar van Mobilize Financial Services

1 Om de ontwikkeling van de geconsolideerde omzet bij constante wisselkoersen te analyseren, herberekent Renault Group de omzet voor de huidige periode door de gemiddelde wisselkoersen van de voorgaande periode toe te passen.

2 Zie de volledige definitie van vrije kasstroom autodivisie op pagina 10.

3 Onder voorbehoud van een voorstel van de Raad van Bestuur van MFS en goedkeuring door de Algemene Vergadering van Aandeelhouders.

4 Gemiddeld 3,9% tussen 2005 en 2025.

5 Vergeleken met het historische gemiddelde van €0,6 miljard per jaar tussen 2005 en 2025.

François Provost, CEO van Renault Group: “Onze resultaten voor 2025, in een uitdagende marktomgeving, tonen de inzet van onze teams om consistente topprestaties te leveren binnen de auto-industrie. Deze prestaties onderstrepen de kracht van onze fundamenten en onze wendbaarheid. Bovenal bevestigt dit succes onze solide productstrategie en de kracht van onze merken, zoals erkend door onze klanten.”

“Over enkele weken zullen we onze strategie uiteenzetten, gericht op de groei van ons bedrijf en het versterken van de veerkracht van ons operationele en financiële model. We positioneren ons om de toekomst met vertrouwen en ambitie tegemoet te gaan, met als doel Renault Group te verankeren als een toonaangevende speler en waarde te creëren voor onze stakeholders.”

Het vervolg van dit persbericht gaat verder in het Engels

Boulogne-Billancourt, February 19, 2026

Commercial performance

- In 2025, Renault Group sold 2,336,807 vehicles worldwide (+3.2% in a market up 1.6%), with all its three complementary brands outperforming the market:

- In Europe, Renault Group is on the podium of OEMs:

- Renault brand #1 French car brand worldwide, and #2 in Europe (PC + LCV[1])Dacia #2 in retail PC in Europe, with Sandero first best-selling passenger car in Europe across all channelsAlpine exceeded 10,000 registrations for the first time, more than doubling versus 2024

- Successful launches:

- in Europe with Renault 5 (#1 EV B-seg in Europe), Renault Symbioz (Renault’s best-selling full hybrid model), Dacia Bigster (best-selling C-SUV to retail customers in H2 2025), and

- continued international expansion with Renault Koleos (3# D-SUV HEV in South Korea) and Renault Kardian (almost 50,000 units sold)

- In Europe, Renault Group is on the podium of OEMs:

- Electrification offensive in PC Europe:

- Renault Group is continuing its electrification offensive, with strong growth in both EVs (+77.3%) and HEVs (+35.2%). Electric and HEV mix reached respectively 14% and 30% of total sales

- Renault brand leads the path in EV thanks to its new models to reach 20.3% EV mix (EV sales +72.4%), while maintaining a strong focus on HEV sales (+17.1%)

- Dacia HEV sales increased by 122.0% compared to 2024

- Strong focus on value:

- Sales to retail customers in Europe[3] represented nearly 60% of the Group PC sales (+17 points versus the market average) with Dacia Sandero, Dacia Duster and Renault Clio in the top 5 of this categoryC-segment and above at 31% for Renault Group PC sales in Europe (+1.0 point)

- A rigorous approach to residual values, 5 to 12 points higher than European competitors[4]

Financial results

The consolidated financial statements of Renault Group and the company accounts of Renault SA at December 31, 2025, were approved by the Board of Directors on February 18, 2026, under the chairmanship of Jean-Dominique Senard.

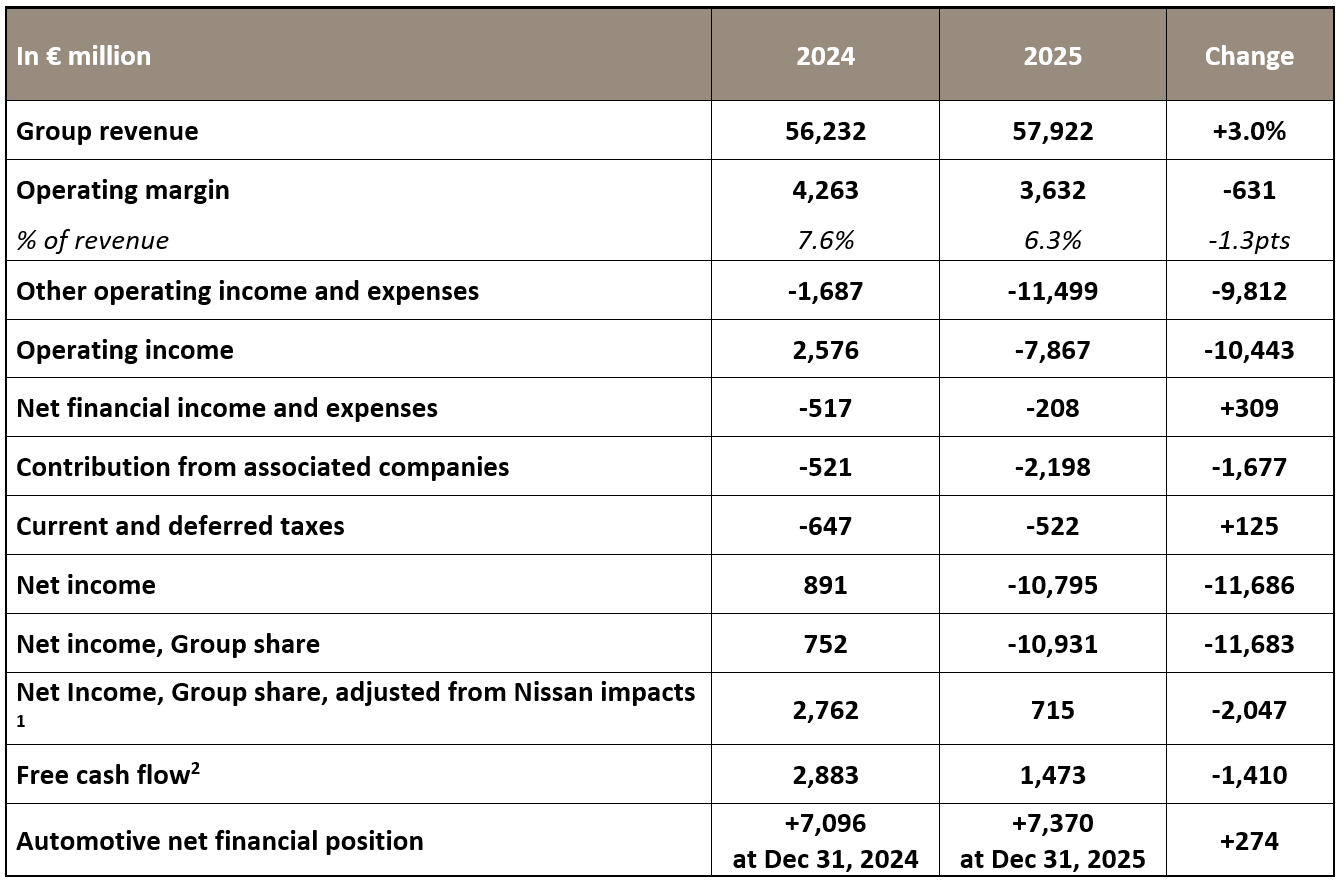

Group revenue reached €57,922 million, up 3.0% compared to 2024. At constant exchange rates[5], it increased by 4.5%.

Automotive revenue stood at €51,442 million, up 1.8% compared to 2024. It included -1.6 points of negative exchange rates effect (-€814 million) mainly related to the devaluation of the Turkish lira and Argentinean peso. At constant exchange rates3, it increased by +3.4%. This evolution was mainly explained by the following:

- A positive volume effect of +0.7 points. The 3.2% increase in registrations was partially offset by a lower restocking within the dealership network in 2025 compared to 2024.

As of December 31, 2025, total inventories of new vehicles stood at a healthy level to operate and represented 539,000 vehicles, of which 442,000 vehicles at independent dealers and 97,000 at Group level. - A positive product mix effect of +3.2 points thanks to our recent launches (Dacia Bigster, Renault Symbioz, Renault 5, Alpine A290, Renault 4, Renault Koleos…). This effect will continue to be supportive in 2026 with new launches.

- A small negative price effect of -0.2 points driven by market conditions in Europe that remain challenging with commercial pressure. Some of the negative currency impacts were offset by price increases. In line with its value‑over‑volume strategy, the Group’s pricing approach maintains a strong emphasis on residual values, which are a key driver of long‑term performance.

- A negative geographic mix of -0.5 points, mainly explained by the growth of sales outside Europe.

- A slight negative effect of sales to partners of -0.1 points. This evolution is primarily explained by the one-off R&D billings to partners in H1 2024 and the deconsolidation of Horse’s powertrains sales to partners at the end of May 2024, partly compensated by the positive effects of programs with our partners and the impact of the integration of RNAIPL (Renault Nissan Automotive India Private Ltd) into the consolidation perimeter since August 1, 2025.

- An “Other” effect of +0.3 points, mostly driven by the performance of parts and accessories and distribution activity.

The Group posted an operating margin of €3,632 million, representing6.3% of revenue, to be compared to €4,263 million and 7.6% in 2024.

Automotive operating margin stood at 4.2% of Automotive revenue, or €2,184 million, compared to €2,996 million in 2024. This evolution was mainly explained by the following:

- An impact of foreign exchange of -€282 million, mostly attributable to the negative effect of the Argentinean peso. The Turkish lira positive impact on production costs was offset by the increase of the Group sales in Türkiye.

- A positive volume effect of +€186 million.

- Price/mix/enrichment and costs effects combined represented -€341 million. This evolution reflects increased commercial pressure, especially in Europe, together with a higher EV mix and increased international sales. It also encompasses a negative effect from lower LCV sales, for which margins are superior to the Group average. It was partly offset by an efficient cost management program. The latter includes the achievement of the target of €400 reduction on variable cost of goods sold (COGS) per vehicle in 2025 notably thanks to a strong purchasing performance, starting to benefit from the synergies on powertrains delivered by Horse Powertrain. It was counterbalanced to a limited extent by higher warranty costs (-€160 million).

- R&D posted a negative impact of -€87 million, primarily due to an unfavorable comparison base with non-recurring R&D billings to partners in H1 2024.

- SG&A improved by +€59 million, thanks to strict control of expenses.

- “Other” effect stood at -€59 million.

- Horse (deconsolidated since May 31, 2024): -€279 million deconsolidation impact in 2025 compared to 2024, detailed in 2025 H1 results press release.

The contribution of Mobilize Financial Services (Sales Financing) to the Group’s operating margin reached €1,468 million versus €1,295 million in 2024, mainly driven by the development of financing and service offers as a key leverage of Renault Group marketing strategy, particularly for electrified vehicles.

Other operating income and expenses were negative at -€11.5 billion (vs -€1.7 billion in 2024). It included the non-cash loss linked to the change of the accounting treatment of Renault Group’s stake in Nissan for -€9.3 billion, impairments for -€0.9 billion on vehicle developments and specific production assets and -€0.4 billion of restructuring costs.

After considering other operating income and expenses, the Group’s operating income stood at

-€7,867 million compared to €2,576 million in 2024.

Net financial income and expenses amounted to -€208 million compared to -€517 million in 2024. Hyperinflation in Argentina had a lower negative impact in 2025 compared to 2024.

The contribution of associated companies amounted to -€2,198 million compared to -€521 million in 2024. It included Nissan’s contributions for -€2,331 million, which no longer affects the result since the change in accounting method (June 30, 2025), and the contribution of Horse Powertrain Limited for €245 million.

Current and deferred taxes represented a charge of -€522 million, including -€24 million related to the French exceptional surtax, compared to a charge of -€647 million in 2024. The effective tax rate stood at 42%. Its evolution in 2025 is significantly impacted by the lack of recognition of deferred taxes on expenses and on tax losses, particularly in France.

Thus, net income, Group share, was -€10,931 million (or -€40.0 per share).Net income, Group share, excluding Nissan impacts[6] was €715 million.

The cash flow of the Automotive business reached €4,744 million in 2025. It included a €300 million dividend from Mobilize Financial Services, with €150 million related to the 2024 financial year and €150 million interim dividend related to the 2025 financial year.

Excluding the impact of asset disposals, the Group’s net CAPEX and R&D total spending stood at €4,012 million i.e. 6.9% of revenue compared to 7.2% of revenue in 2024. Assets disposals amounted to €71 million, compared to €94 million in 2024. Group’s net CAPEX and R&D amounted to 6.8% of revenue including asset disposals.

Automotive free cash flow[7] stood at €1,473 million, including -€300 million of restructuring charges. It included a negative change in working capital requirement (WCR) of -€190 million. It underscores the Group’s willingness to have a healthy and sustainable working capital requirement management. In this context, Renault Group aims to unwind, in 2025 and 2026, the significantly positive €844 million change in WCR recorded at the end of 2024.

The Automotive net cash financial position stood at €7,370 million on December 31, 2025, compared to €7,096 million on December 31, 2024. This evolution was driven by the strong free cash flow and included -€697 million of dividend paid to shareholders, -€186 million of net financial investments (mainly Free To X), and the impact of RNAIPL’s acquisition and consolidation for +€76 million.

Automotive liquidity reserve at the end of December 2025 stood at a high level at €17.7 billion versus €18.5 billion on December 31, 2024.

Dividend

The proposed dividend for the financial year 2025 is €2.20 per share,stable versus last year in absolute value. It would be paid fully in cash and will be submitted for approval at the Annual General Meeting on April 30, 2026. The ex-dividend date is scheduled on May 8, 2026 and the payment date on May 12, 2026.

2026 financial outlook: resilience in a complex environment

- In 2026, Renault Group is pursuing its product offensive:

- The Group will renew and enlarge its offer in Europe focusing on EV and hybrid, with among others: New Renault Clio, Renault Twingo E-Tech electric, Trafic van E-Tech, a new A‑segment electric Dacia, a new C-segment ICE & hybrid Dacia, and Alpine A390.

- And accelerate its international growth, notably with Renault Boreal (C-SUV) in Latin America and Türkiye, Renault Duster in India, Renault Filante (E-SUV) in South Korea and overseas markets, and a new pick-up Renault in Latin America.

Regarding the financial outlook for the full year 2026, Renault Group is aiming to achieve:

- A Group operating margin around 5.5% of Group revenue

- An Automotive free cash flow around €1.0 billion

In 2026, international expansion, increasing sales to partners, the growing share of electric vehicles and the consolidation of RNAIPL[8] on a full year basis will drive revenue growth although being dilutive on margins. Cost reduction remains a key priority in 2026 and in the years ahead.

2026 Automotive free cash flow should include €350 million dividend from Mobilize Financial Services[9] (vs €300 million received in 2025). The Group expects a negative change in working capital requirement in 2026, to continue to unwind the positive change in working capital requirement recorded at the end of 2024.

Medium-term financial outlook: sustain robust and resilient financial results

The strategic roadmap will be presented during the Strategy Day on March 10, 2026 and executed building upon the following:

- Product & customer experience: Renault Group aims to deliver a 2nd successful line‑up in Europe and be a contender in high-potential markets (India, Latin America) while providing to its customers a high-quality and differentiating end-to-end experience along vehicle lifetime.

- Technology & innovation: Renault Group aims to deliver a full set of techno bricks for EV and software and will write the next chapter of the success story on hybrids.

- Operational excellence: Renault Group aims for excellence in the management of its operations to catch up Chinese OEMs on innovation, cost and speed.

- Engaged with stakeholders: Renault Group aims to pursue proactive dialogue and build set of actions with all stakeholders: employees, suppliers, dealers and partners. Regarding partnerships, Renault Group aims to be strong on a standalone basis, with partnerships as boosters for competitiveness.

Today, the Group unveils its medium-term financial outlook.

In a highly challenging environment, the Group aims to create value with consistency and predictability, through a disciplined and realistic approach. It targets[10] a sustainable robust operating margin and a strong free cash flow generation:

- Group operating margin between 5% and 7% of Group revenue over the medium term. The lower end of the margin range being tangibly above the historical margins [11].

- Automotive free cash flow ≥€1.5 billion per year on average over the medium term[12] including circa €500 million dividend[13] per year on average from Mobilize Financial Services.

Sustainable robust operating margin

Products and expansion in international markets will be drivers of growth sustained by the acceleration of the Group’s transformation to increase speed, agility, efficiency and simplicity.

Renault Group assumes its total revenue to grow mid-single digit (CAGR[14]) over the medium term. This growth will be supported by both the Automotive business and Mobilize Financial Services.

The plan is designed to strengthen Renault Group on a standalone basis especially in Europe and be open to partnerships as boosters for competitiveness especially outside Europe.

Cost reduction will remain a key priority across the Group and will be achieved through variable cost performance and fixed cost discipline:

- Variable costs: Variable costs per vehicle (COGS) are expected to be reduced by around €400 per year on average, thanks notably to technology improvement, Horse Powertrain competitiveness, and close collaboration with suppliers.

- Fixed cost discipline, with strong focus on productivity:

- R&D Capex and supplier entry ticket expenses: new projects’ entry ticket reduction by up to

-40% compared with previous generation, notably thanks to 2-year vehicle development time becoming the standard and processes reshuffling.

- SG&A expenses: stable over the medium term.

- R&D Capex and supplier entry ticket expenses: new projects’ entry ticket reduction by up to

As a consequence, Renault Group will maintain a stable cash fixed cost base over the medium term, allowing a cautious break-even point management.

Strong free cash flow generation

The free cash flow generation over the medium term will be supported by enhanced profitability.

The Group will invest in product and innovation while maintaining a very disciplined approach to reducing entry tickets. The R&D Capex and supplier entry ticket spending will remain below 8% of Group revenue.

Regarding the dividend received from Mobilize Financial Services, the Group anticipates it to be aligned with the historical average, meaning around 500 million euros[15] per year on average over the medium term.

From 2027 onwards, the Group should receive a dividend from Horse Powertrain Limited[16].

Altogether, this is securing the sustainability of cash inflows hence protecting the solidity of the balance sheet.

Disciplined and balancedcapital allocation policy

Renault Group remains committed to implementing a disciplined and balanced capital allocation:

- Invest in priority into the product to drive future growth. The Group will also pursue a disciplined and targeted financial investment strategy with priority to reinforce its core automotive business and in businesses providing both an industrial rationale and a high return on capital employed (ROCE).

- Preserve a strong balance sheet in order to protect its investment grade profile while maintaining a strong liquidity reserve.

- Return value creation to stakeholders:

- To employees, through profit sharing mechanisms and dedicated employees’ shareholding programs. The Group ambitions to grow its employee shareholding towards 10% of its capital in the long term.

- To shareholders, through an attractive dividend policy with a progressive increase in the dividend per share in absolute value.

In terms of ROCE, Renault Group’s ambition is to deliver a high ROCE trending towards 25% in the medium term, supported by its asset-light organization, its disciplined approach to R&D Capex and a sustained focus on value‑accretive businesses.

Renault Group’s consolidated results

(1) FY 2024: +€211 million of Nissan’s contribution in associated companies and -€1,527 million of capital losses on Nissan’s shares disposals and -€694 million of impairment of investment in Nissan.

FY 2025: -€2,331 million of Nissan’s contribution in associated companies, and -€9,315 million loss resulting from the evolution of the accounting treatment for the investment in Nissan.

(2) Automotive free cash flow: cash flows after interest and tax (excluding dividends received from publicly listed companies) minus tangible and intangible investments net of disposals +/- change in the working capital requirement.

Additional information

The consolidated financial statements of Renault Group and the company accounts of

Renault SA at December 31, 2025 were approved by the Board of Directors on February 18, 2026.

The Group’s statutory auditors have conducted an audit of these financial statements, and their report will be issued shortly.

The earnings report, with a complete analysis of 2025 financial results including condensed financial accounts, is available at www.renaultgroup.com in the “Investors” section.

2025 Financial Results Conference

Link to follow the conference at 8am CET on February 19th, 2026 and available in replay: events.renaultgroup.com/en/

[1] PC + LCV: Passenger Cars + Light Commercial Vehicles.

[2] Outside Europe.

[3] France, Italy, Spain, Germany and United Kingdom.

[4] 22 main brands PC segment, France, Italy, Spain, Germany and United Kingdom. Residual values on sales with buy-back commitments.

[5] In order to analyse the variation in consolidated revenue at constant exchange rates, Renault Group recalculates the revenue for the current period by applying average exchange rates of the previous period.

[6] Nissan’s impacts in 2025: -€2,331m of Nissan’s negative contribution in associated companies, -€9,315m loss resulting from the evolution of the accounting treatment for the investment in Nissan recorded in other income and expenses.

[7] See Automotive free cash flow full definition on page 10.

[8] RNAIPL: Renault Nissan Automotive India Private Ltd.

[9] Subject to MFS Board of Directors proposal and Shareholders’ General Meeting approval.

[10] At constant accounting standards, excluding the potential impacts of IFRS18 which are being considered for a first application in 2027.

[11] 3.9% on average between 2005 and 2025.

[12] Compared to historical average of €0.6 billion per year on average between 2005 and 2025.

[13] Subject to MFS Board of Directors proposal and Shareholders’ General Meeting approval.

[14] CAGR: Compound Annual Growth Rate.

[15] Subject to MFS Board of Directors proposal and Shareholders’ General Meeting approval.

[16] Subject to Horse Powertrain Limited Shareholders’ General Meeting approval.